The latest in our series based on SAFIRE, a proposed system using foresight to develop policy for Research and Innovation relationships for the EU, is a review of the Middle East and North Africa. Our aim is not to review what the report contains, but to identify signs of progress, or confounding issues, which may affect the scenarios for the region.

The original SAFIRE Report is available via the link here. Four global scenarios provide the structure of a “gameboard”. These were then expanded into scenarios of each of the 10 Regions – the scenario reports for each Region can be found within Chapter 3 of the report. At a workshop, Regional experts then examined how their Region might journey through the scenarios over time.

The Report was published in autumn 2021, but we continue to monitor developments and trends in each of the ten Regions. So these blogs, rather than simply recycling the content of the Report, look at the trends that might influence how each Region might move across the scenario “gameboard” over the next 20 years.

Driving Change in MENA

MENA is neither a region nor is it typical

We start with two general points. The Middle East and North Africa is not really a region. Unified (by politicians in the West) by Islam and the Arabic language, the superficial unity disguises widespread differences in social, political, economic and other factors – indeed, the full STEEPLE mix. It is better to think of three regions – North Africa, the Gulf, and the Levant (though this name itself comes freighted with imperialist overtones).

Our study, however, brought all three subregions together, which, whilst useful, also in some respects disguised the essential disunity which is fundamental to understanding what actually may happen.

We also, for various reasons, excluded the explicit mention of Israel (neither Islamic nor Arabic), Turkey (nominally secular and Turkish speaking) and Iran (traditionally not included in MENA for cultural, geographic and other reasons).

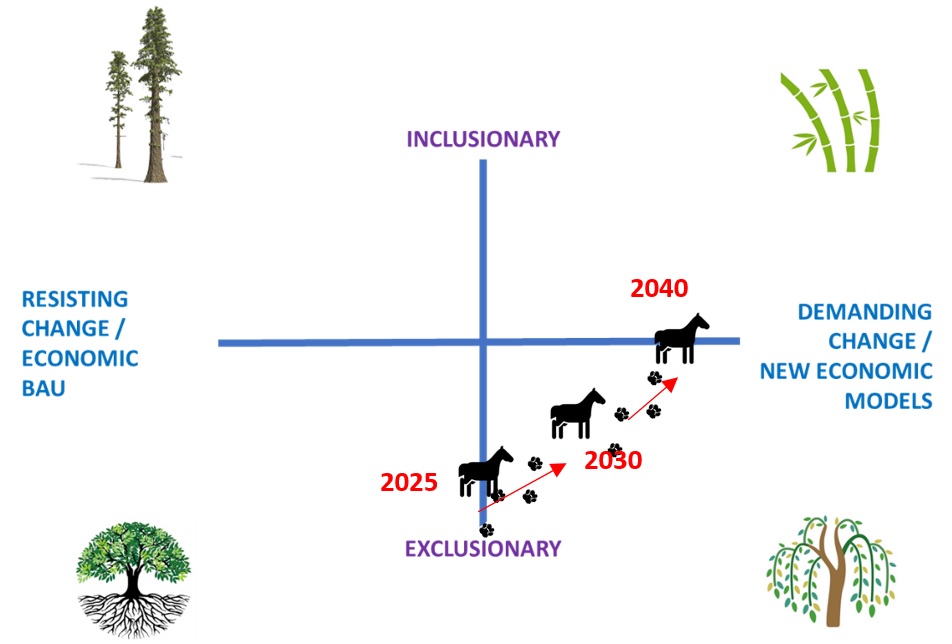

The region is also not typical. The general view of the overall direction of travel within the scenarios tended towards our “Oak” scenario – exclusionary and resisting change. However, if you look at the scenario frame above, which includes the two-phase scenario project we developed for this project (the Journey Game), you’ll note that whilst the region starts on the border of Oak, our participants thought that the region would, between 2025 and 2040, move steadily towards “Bamboo” – demanding change and inclusionary. This is exceptional in the context of the SAFIRE project – and implies the region has a more hopeful future than it sometimes seems it might.

Recent events, however, may prove a challenge to this positive projection.

The influence of Israel, Turkey and Iran

No region is isolate to itself, still less one as complex as MENA. Still less again, when it has three powerful neighbours which act as poles of disruption.

Israel is potentially a contributor to speeding up travel to Bamboo. The recent visit of Israel’s president Herzog to the UAE is the clearest example. For those of us who have been watching the region for years, seeing an Emirati band play the Israeli national anthem in front of President Herzog and Crown Prince Mohammed Bin Zayed, in the UAE national palace, is a concrete example of a radical change in approach from all sides. The “Abraham Accords” that led to this meeting are groundbreaking.

A substantial driver in the accords is the region’s response to Iran, whose influence across the region remains deeply felt. Its explicit support for disruptive forces in Lebanon and Syria and its covert support more widely, coupled with its nuclear ambitions, remain a source of tension. Without a revolutionary change in the country’s government and outlook, we anticipate that Iran’s influence will continue to do two main things: force rapprochement between Israel and the Sunni states; and be a source of instability across the region.

President Erdoğan continues to drive an expansionist foreign policy in Turkey. Whilst this has many names (among the least useful being “neo-Ottomanism”), Turkey’s desire for a place in the world, particularly in its near abroad, has led to an involvement in Syria, clashes with the Kurds, direct battlefield confrontations with Russia, and an overt intervention in the recent Armenia-Azerbaijan conflict. The undoubted success of Turkey’s military equipment, especially the drone technology in the TB2 Bayraktar, and Erdoğan’s militarised foreign policy, are both disruptive. However, their success will inevitably mean they will continue. Even a change of government in Turkey is unlikely to signal a return to Ataturk’s “peace at home, peace in the world” doctrine.

Second-order effects from the invasion of Ukraine

Harold Macmillan’s line about “Events, dear boy, events” being the statesman’s greatest challenge has become trite. However, the last two months have proved its truth.

There is nothing so diverting to the global order as a European war. Powerfully armed, nationalistic states and groupings (including NATO and the EU), fighting each other in Eurasia, disrupt almost everything, almost everywhere. As long as the conflict remains between Russia and Europe, however, it should not directly affect the region even if it goes very badly wrong.

Except, of course, it does. Not in the boots-on-the-ground sense, though Ukraine’s recent withdrawal of its peacekeeping forces is an unpleasant harbinger of what may happen if this turns into a general European war. It is the second-order effects that matter, and especially two.

Grains

The impact on grains exports to the region stemming from Russia’s invasion of Ukraine is profound.

- Turkish agriculture ministry data indicates that the country imported almost half of its wheat needs in 2020, mainly from Russia with 64 percent of imports, and Ukraine at 13.4 percent.

- Lebanon consumes approximately 450,000-550,000 tonnes of wheat every year and imports 60 percent of its wheat from Ukraine.

- Between 2020 and 2021, Egypt imported most of its wheat – 12.5 million tonnes – from Russia and Ukraine. The price of bread is political in Egypt, and at least 70 percent of the country’s 102 million population rely on subsidised bread. Almost 85 percent of Egypt’s wheat imports in 2020-21 came from Russia and Ukraine.

- Ukraine, the world’s fifth largest wheat producer in 2019, exports most of its output to North African states.

- Wheat makes up almost half of Tunisia’s overall cereal imports. These come from a wide range of suppliers, on top of which are Ukraine and Russia.

- “Russia is Tunisia’s traditional ally when it comes to wheat imports,” Tunisian political commentator Najeh Missaoui told MEE. “The Tunisian government has already started searching for alternatives.”

- Having previously relied on European wheat, Algeria imported it from Russia last year for the first time in five years, due to changes in its import specifications.[1]

Historically, the one thing that causes significant disruption in the region is bread. Subsidised, to one degree or another, virtually everywhere, bread is the fundamental foodstuff of the Middle East and North Africa, and price rises or absence leads to civil disorder.

Civil disorder will affect our scenarios. Should the war be short, then governments in the region should survive. Suppose it is long, or international sanctions on Russia remain sustained. In that case, countries within the region will collapse into themselves as their public search for bread. The potential of unrest affects all North Africa and the Levant, the Gulf only really being exempt through its wealth and relatively smaller populations.

Oil

The global economy is in an intensely fragile state. Two years of Covid, the still unresolved effects of the 2008 global financial crisis, and supply chain disruptions have led to governments pumping money into economies, to the point where it must be questionable how long it can be sustained. An oil price shock, caused by the removal from the international markets of Russian oil, will be another blow to the global system. Releasing oil from strategic reservescan only support prices for so long.

Gulf states are maintaining their support for the OPEC+ agreements at present. No further crude is to be brought onto the market. But Brent crude has risen 60% in 2022, and the previous peak of $147/barrel (2008) is almost sure to be breached.

This is good news only for one of our subregions. The combination of higher oil prices and much less wheat is potentially highly disruptive for the rest.

Where now?

Our scenarios for MENA were fundamentally optimistic. Our Journey Game direction of travel was more so. Nothing within the region has changed to alter those scenarios – in fact, with the rapprochement between Israel and its neighbours, we could be more confident than before.

But externalities are really going to hurt. Power prices will rise. Wheat will become scarce. The fundamental difference in world view between Iran and the region will remain and intensify, even should the nuclear talks be successful. We move from some confidence to some nervousness.

Written by Jonathan Blanchard Smith, SAMI Fellow and Director

The views expressed are those of the author(s) and not necessarily of SAMI Consulting.

Future-prepared firms outperform the average by 33% higher profitability and 200% higher growth. SAMI Consulting brings 30 years of experience delivering foresight, futures and scenario planning – enabling companies and organisations make “robust decisions in uncertain times”. Find out more www.samiconsulting.co.uk.

If you enjoyed this blog from SAMI Consulting, the home of scenario planning, please sign up for our monthly newsletter at newreader@samiconsulting.co.uk and/or browse our website at https://www.samiconsulting.co.uk