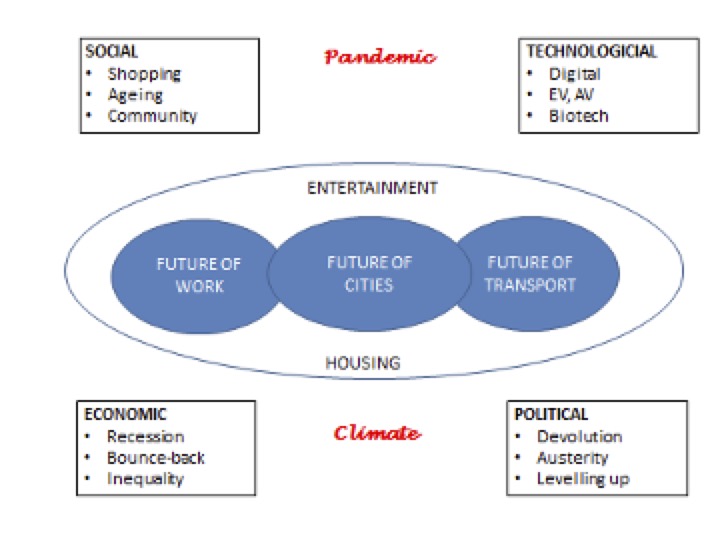

In this final post on the Future of Cities, we examine the Political decisions that will shape their development. As we noted last time, the economic situation caused by the pandemic forms the backdrop against which political decisions are taken.

Recession – recovery

Forecasts of GDP growth vary widely over the next few years because of the direct impacts of the coronavirus pandemic and the extended recession which is expected to follow. The World Bank’s “Global Economic Prospects” report in June envisaged deep recessions leaving lasting scars through lower investment, an erosion of human capital through lost work and schooling, and fragmentation of global trade and supply linkages. Countries hit hardest by the pandemic – notably the UK – will have lower growth.

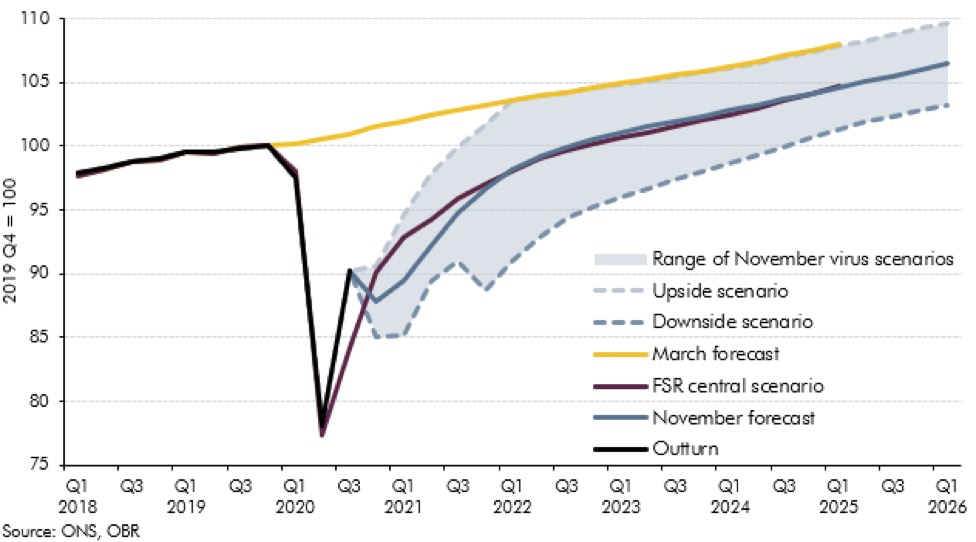

The November OBR forecast estimated a fall of GDP during 2020 of 11.1%. There are a range of scenarios depending on the course of the pandemic, but the November forecast of GDP remains 10% below the January 2020 level.

Chart 2.12: Real GDP paths

The central forecast returns to January 2020 levels in Q3 2023, and remains about 4% points lower than the March forecast at least until Q1 2026.

For the UK, the country’s departure from the EU adds extra uncertainty. Whilst some seem convinced that Brexit will lead to an upsurge in entrepreneurialism and economic prosperity, the official forecasts point in the opposite direction.

Austerity?

The key political decision will be how fast to pay down the higher debt incurred by the emergency measures, and in what way. The November OBR forecast put borrowing at £394 billion in 2020/21 and £100m 2024/25. These decisions will hugely influence the speed, scale and shape of the recovery.

In the EU there seems to be an appetite for a substantial continued investment funded by borrowing, though some commentators believe even this is insufficient. In the UK, conversely, most discussion has revolved around increased taxation versus more spending cuts.

Paul Johnson, the director of the Institute for Fiscal Studies (IFS) thinktank, said: “It seems more likely than not that spending will end up significantly higher than set out today [25 November 2020], and so borrowing in 2024-25 will be considerably more than the £100bn forecast by the OBR. Either that or we are in for a pretty austere few years once again, or for some significant tax rises.” In his November Spending Review, the Chancellor announced a public sector pay freeze (apart from the NHS), giving an early indication of his intentions. More recently, Tory MPs have expressed concern about possible tax rises and the Chancellor said there would not be a “horror show of tax rises with no end in sight”.

The TUC and public service union Unison have argued that the UK’s most deprived metropolitan areas had to “shoulder the burden of austerity” between 2010 and 2019.

Analysis by IFS and Centre for Cities of central government funding for local councils in England since 2010 shows a huge gap between urban and rural areas. Overall, councils in England are spending £7.8bn a year less on key services than they did in 2010, which equates to a cut of £150m a week.

Clearly, if the Government repeats that approach, scope for Cities to invest in new technology and infrastructure will be minimal, as obligations to cover statutory services such as social care will have to take priority.

“Levelling up”?

A stated priority of the UK Government, perhaps thrown off course for the present by the pandemic, is “levelling up” – reducing regional inequality. It’s not entirely clear what the term will mean, but a new group, the “levelling up taskforce” – which includes many of the new “red wall” MPs – is suggesting three key tests:

- areas that have seen the lowest growth in earnings, should see earnings rise faster than they have in recent years;

- areas with the worst unemployment rate should converge with the national average

- areas with the lowest employment rate should also catch up with the national average.

Unemployment is highest in the North East (October 2020) at 6.6%, though London is at 6.3%. It is lowest in the South-East and Northern Ireland (3.9%)

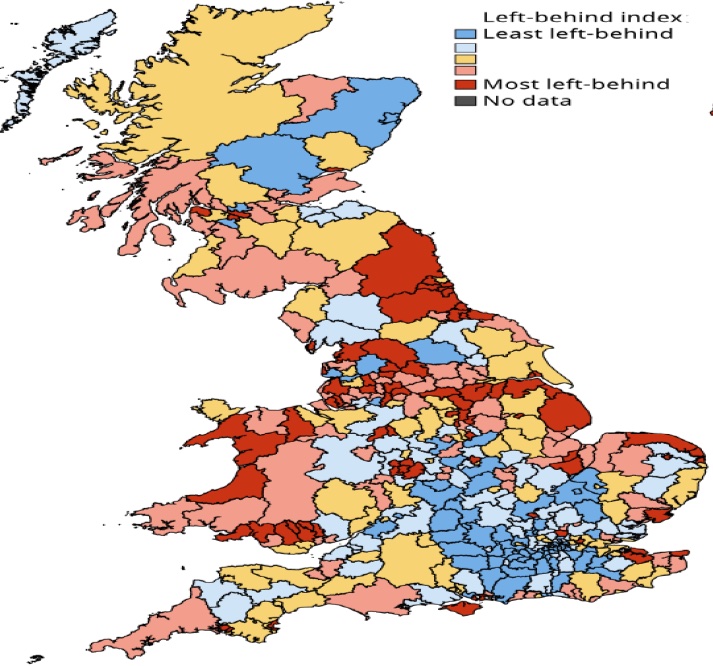

The IFS created a “left-behind” index with components of employment, formal education, incapacity benefit and pay. Nearly all of the North-East region, much of the metropolitan North, and large parts of Wales are in the “most left-behind” category.

“Levelling up” in a general environment of debt reduction would put a huge strain on other, more traditionally Conservative, areas

The IFS suggest that the economic impact of Brexit is likely to impose a particularly high economic cost on some groups, such as less-educated male workers in blue-collar jobs. Many of these are concentrated in ‘left-behind’ areas.

The November National Infrastructure Strategy also addresses “levelling up” in areas such as strategic roads and rail, flood defences and broadband. There is a ‘Levelling Up Fund’ of £4.2bn over five years for the largest city regions outside London, which will be invested in relatively small local infrastructure projects across England and managed by three government departments (MHCLG, DfT and HMT).

Devolution.

Potentially going hand-in-hand with “levelling up” is devolution of decision-making. The white paper on devolution and local recovery, which was expected in September, has been shelved until later this year.

The “Levelling up Fund” is a competition for a pot of money, allocated from the centre, rather than devolution. The Institute for Government is concerned that “disagreements with combined authority mayors and local authorities over the Covid-19 response have stymied the government’s enthusiasm for devolution”.

Local Mayors argue that devolution allows for a more effective allocation of resources from a single pot than central Government can achieve. We will watch with interest how this debate plays out.

Overall, we see a tension between social changes and new technology, which offer the prospect of novel city developments and innovative services, against the limitations imposed by the pandemic recession and associated political reactions. This tension could be resolved to a degree by greater devolution, but how radical central Government is prepared to be we have yet to see.

Globally, we think the fine images of visionary, inclusive, smart green cities will, when faced with the economic facts of pandemic recession and the chaotic reality of places like Lagos, Kinshasa, Dhaka and Bangalore, become to be seen as idealistic, impractical, unsustainable, and expensive.

Written by Huw Williams, SAMI Principal

The views expressed are those of the author(s) and not necessarily of SAMI Consulting.

SAMI Consulting was founded in 1989 by Shell and St Andrews University. They have undertaken scenario planning projects for a wide range of UK and international organisations. Their core skill is providing the link between futures research and strategy.

If you enjoyed this blog from SAMI Consulting, the home of scenario planning, please sign up for our monthly newsletter at newreader@samiconsulting.co.uk and/or browse our website at https://www.samiconsulting.co.uk

Image by Tumisu from Pixabay