The future prosperity of the United Kingdom depends in no small part on Financial Services, mostly based in London. This blog therefore sets out one scenario for the future of London. A subsequent blog will set out an alternative future.

Decline in the seventies

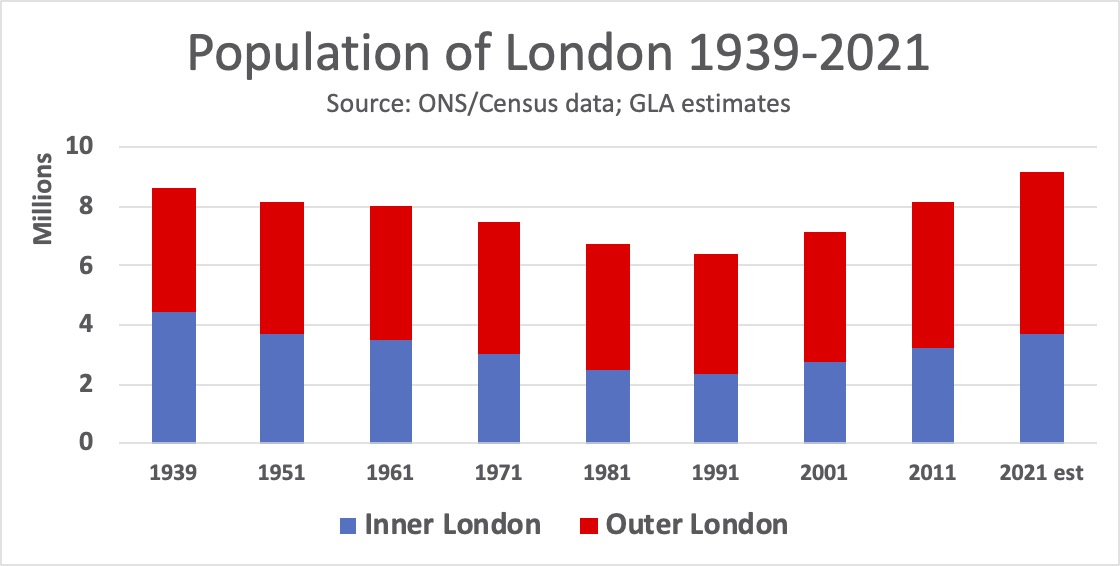

In the 1970’s, big cities did not fare well. New York famously faced bankruptcy, and London was losing population. The docks had moved down river to Tilbury and to Felixstowe. Many factories had moved out of the capital, with jobs and people following them. The population of London reached a low point in the 1980’s. (See chart of ONS data and 2021 projection.)

In the 1970’s, big cities did not fare well. New York famously faced bankruptcy, and London was losing population. The docks had moved down river to Tilbury and to Felixstowe. Many factories had moved out of the capital, with jobs and people following them. The population of London reached a low point in the 1980’s. (See chart of ONS data and 2021 projection.)

London as a financial centre was similarly weak. The 1976 Sterling crisis forced Britain to apply for an emergency loan from the IMF. And the chancellor at the time, Dennis Healey, railed against the power of the “Gnomes of Zurich”, who had the financial clout to take positions against sterling, thwarting his attempts to support the pound.

Growth in the nineties

But then something extraordinary happened. London started to grow again.

- The “Big Bang” of 1986 deregulated the London Stock Exchange, allowing full-service investment banking, and enabling inward investment by big American banks and other global players.

- The growth of the Eurobond market helped London to grow as a financial centre.

- Derivatives trading found a natural home in the deregulated free-wheeling markets of London.

Wider economic shifts contributed to London’s growth.

- The UK economy continued its shift from manufacturing to services, which were concentrated in London.

- The predictability of Common Law systems, and the business-friendly commercial courts, helped the English Law to become the preferred standard for the contracts of much international commerce.

- Increasing capacity of rail networks allowed commuting by more people from ever greater distances.

- Co-location effects became more important in the global economy. These applied to London as much as they applied to Silicon Valley. The largest metropolitan areas consistently delivered greater productivity and value added per head.

In the eighties and nineties, London again started to create jobs, sucking in people from across the country and driving up property prices and thereby increasing the wealth of Londoners and bolstering balance sheets.

European scale

These factors were compounded in the nineties and the noughties. The natural hinterland supporting the growth of London expanded from one country to twenty-eight.

- After the EU single market was created in 1993, passporting allowed many global investment banks to service the whole of Europe from a single base in London.

- Free movement of people sucked in people from across the European Union, driving up the population. By 2012, more French people lived in London than in Bordeaux or in Strasbourg.

- The enlargement of the EU in 2004 brought in ten new countries, with poor but mobile young workers seeking opportunities abroad.

- In the financial crash of 2008, EU law protected the free-wheeling financial services ethos of London from the more dirigiste tendencies of continental European finance ministries.

All of these factors led to the current situation where London had become the dominant financial centre in the European time zone, with particular strengths in derivatives trading, investment banking and in fintech.

Current outlook

But we are now in a situation where the growth of London has become highly uncertain. Some commentators expect the population of London to shrink again for the first time in a generation; share trading volumes on the Amsterdam Stock Exchange now exceed those in London; and the future of Financial Services based in the UK has been thrown into confusion by Brexit.

In the remainder of this blog we use three different Futures techniques to explore the implications for London.

Drivers analysis

Most of the most recent drivers of London’s growth listed above are vulnerable to being reversed after Brexit:

- Passporting will no longer apply to UK services. And even if it is allowed, this privilege can be unilaterally withdrawn by the EU at a moment’s notice. Global banks need to set up operations within the EU in order to continue business there. And more and more of their functions will follow.

- The free movement of people that has underpinned the growth of London’s population has ended.

- Whatever arrangement may be negotiated between the UK government and the EU for mutual recognition of regulations, it seems difficult to see how the successors to Merkel and Macron will tolerate un-fettered “Anglo-Saxon capitalism” when that is blamed in Europe as the root cause of the next financial crash. EU law will not protect the UK financial industry again. And crashes are an inevitable result of free-market capitalism.

The only driver listed above which supports the continuing growth of London is that of co-location. The combination of the full range of financial services and the legal and accounting services that underpin London create a powerful feedback loop. But of course, positive feedback loops can work either way: Weakening any component of the virtuous circle weakens the others.

Analogy

One common analogy for the future of London is “Singapore-on-Thames”, where Singapore acts as a hub providing commercial, financial, transport and other services throughout its region. But Singapore’s neighbours in South East Asia are separate less powerful states, with different agendas and no easy vehicle to allow them to act together.

In Europe, trade policy is set at EU level. A more compelling analogy is therefore the relationship between Canada and the USA. The USA is by far the more powerful partner, as evidenced by the unilateral renegotiation of the NAFTA free-trade deal by Donald Trump in 2019. The USA welcomes Canada as a peaceful neighbour on its northern border and as a useful source of primary products (grain, lumber, oil etc.). Congress and the SEC would never tolerate Toronto being the predominant supplier of financial services on the North American continent. They would find some way to use their economic might to wrest control of trading and services and bring that crown back to New York.

War-gaming

The military use scenario planning in tactics. Even the most junior officers are taught to analyse a situation before acting: “What is your situation? What is the most damaging thing the enemy could do? What do you think they’re going to do? What else might they do? What are you going to do?”

In terms of financial services, the worst-case scenario would be that the EU actively uses its economic weight to engineer the growth of continental financial services at the expense of London. It could actively use equivalence, and the threat of its removal, to undermine London’s attractiveness as a financial centre, and as a useful tool to force compliance on the authorities in London.

The EU might also choose to avoid damaging internal conflicts by cooperating between member states. One possible “share-out” could be:

- Share trading and derivatives trading to Amsterdam, where the mercantile tradition is strong

- Insurance and fund management to Frankfurt, which has big national champions already

- Legal services to Paris

- Fin-tech to Berlin, where there is already a strong fintech industry

Conclusions

Looking at the future of London through the lenses of drivers analysis, analogy or wargaming gives similar results. It may take a generation or so, but the expectation must be that London will lose its crown as the predominant financial services metropolis in Europe.

And for those who think that financial services in London are too big and too entrenched to be at risk, just remember what happened to the dockworkers in the seventies. And who hears about the all-powerful Gnomes of Zurich now?

Written by Martin Duckworth, SAMI Principal

The views expressed are those of the author(s) and not necessarily of SAMI Consulting.

Future-prepared firms outperform the average by 33% higher profitability and 200% higher growth. SAMI Consulting brings 30 years of experience delivering foresight, futures and scenario planning – enabling companies and organisations make “robust decisions in uncertain times”. Find out more www.samiconsulting.co.uk.

If you enjoyed this blog from SAMI Consulting, the home of scenario planning, please sign up for our monthly newsletter at newreader@samiconsulting.co.uk and/or browse our website at https://www.samiconsulting.co.uk

Image by Ana Gic from Pixabay

[…] We have analysed some approaches to the future of London in a previous blog. […]